To say peptides have become a hot topic is an understatement. They are not new. Collagen supplements and now GLP-1 are among peptides that have heavy science backing them and tons of users world wide. But now there are more, and they promise incredible benefits. The problem? Regulation and access.

Let's explore this topic together.

Table of Contents

- What peptides actually are and why they're different from everything else in medicine

- The Peptide landscape & categories that matter

- What does it mean for any digital health company?

- The business models winning in peptide therapy

- Final Insights

Peptides are now dividing healthcare and the longevity market between those who call them miracles and those who need more research before believing any claim. The truth, of course, falls somewhere in the middle. With a $USD 87.21 billion market on the horizon, peptides are being called the 21st-century gold rush. And like any other industry, when hype fades, true structure and sound business models are what prevail.

What remains intriguing is this: after so many hard lessons learned from building around GLP-1 (the peptide of the decade) many founders still don't recognize that healthcare demands certain non-negotiable considerations: technology, regulation, and clinical expertise.

Whether it's GLP-1 or any other peptide, the standards are the same. And they can't be compromised, because at the end of the day, striving for longevity is still healthcare and the patient should be at the center of any build.

What peptides actually are and why they're different from everything else in medicine

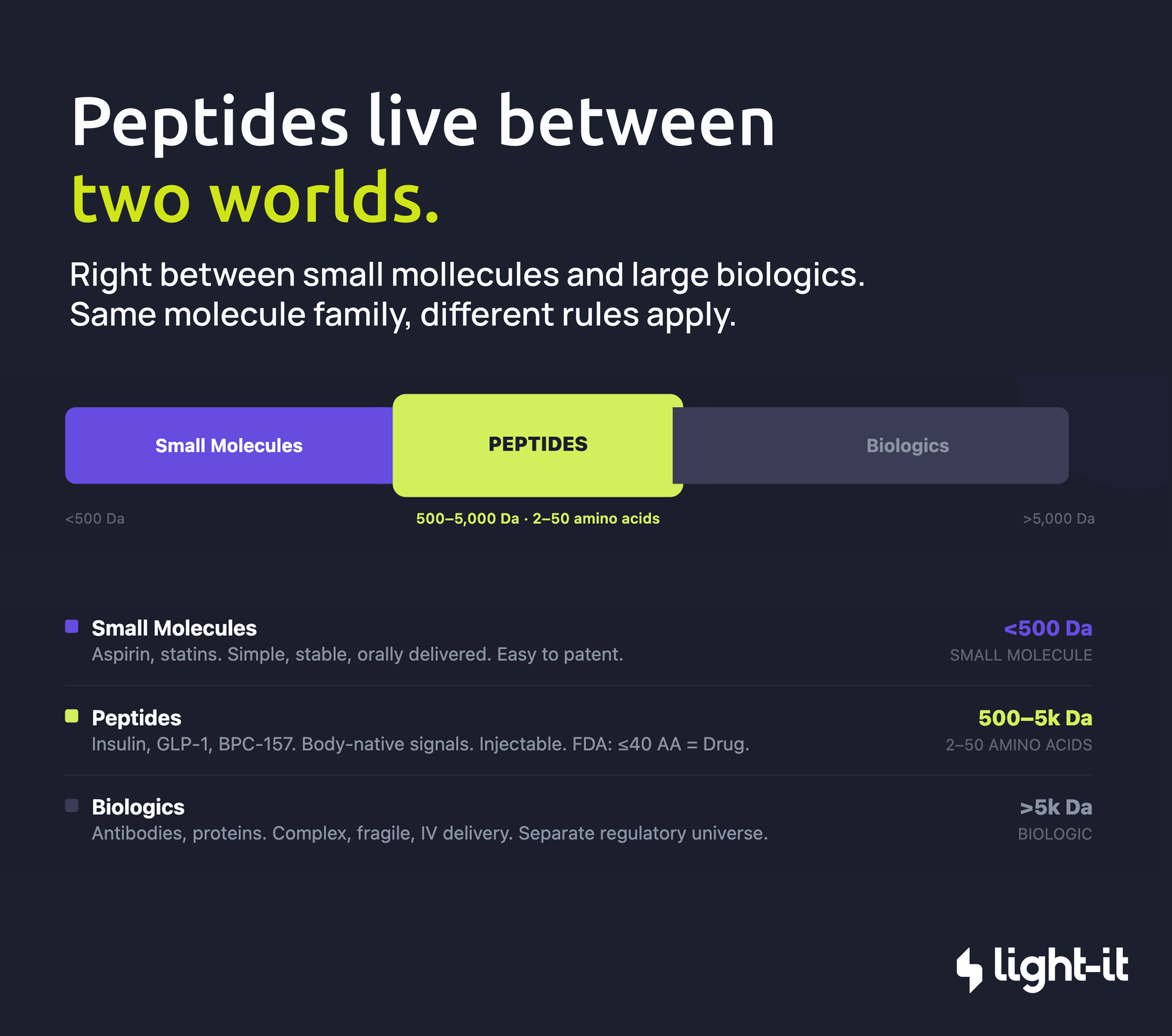

At their core, peptides are short chains of amino acids, held together by peptide bonds. Simple in structure, complex in implication. Biochemistry textbooks draw the line at 2 to 50 amino acids. The FDA draws a different one: 40 amino acids or fewer get regulated as a drug. Anything larger becomes a biologic. Same molecule family, completely different regulatory universe.

What makes peptides genuinely interesting from a business and clinical standpoint is where they sit in the therapeutic spectrum: right between small molecules and large biologics.

Your body already runs on peptides. Insulin, oxytocin, GLP-1, these aren't pharmaceutical inventions, they're native signals your biology already knows how to read. Therapeutic peptides work on that same principle: you're not introducing a foreign substance (when manufactured safely), you're speaking the body's own language, just at a higher volume and for longer than it would naturally sustain.

The Peptide landscape & categories that matter

So what's actually at stake here? The legality of selling peptides isn't a yes or no question. It depends on who's selling, which peptide, and whether a prescription is in the picture.

Most popular peptides (BPC-157, TB-500, Semax, and others) are not FDA-approved. The exceptions are the ones that went through the full pharmaceutical pipeline: insulin, GLP-1 drugs like semaglutide, and a handful of others.

For everything else, there's a distinction worth understanding. A peptide being "legal to compound" is not the same as being FDA-approved. Licensed compounding pharmacies can legally prepare and dispense certain peptides under a physician's prescription, but compounded medications are by definition not FDA-approved products.

Here's how the market actually breaks down:

1. Licensed Compounding Pharmacies: Legal, but narrow

Compounding pharmacies (503A and 503B facilities) can legally prepare and sell peptides, but only with a valid doctor's prescription. No prescription, no sale. And not every peptide qualifies. Pharmacies can only compound peptides that are FDA-approved, Generally Recognized as Safe (GRAS), have a USP monograph, or appear on the FDA’s Category 1 bulk drug substances list (think NAD+ or sermorelin).

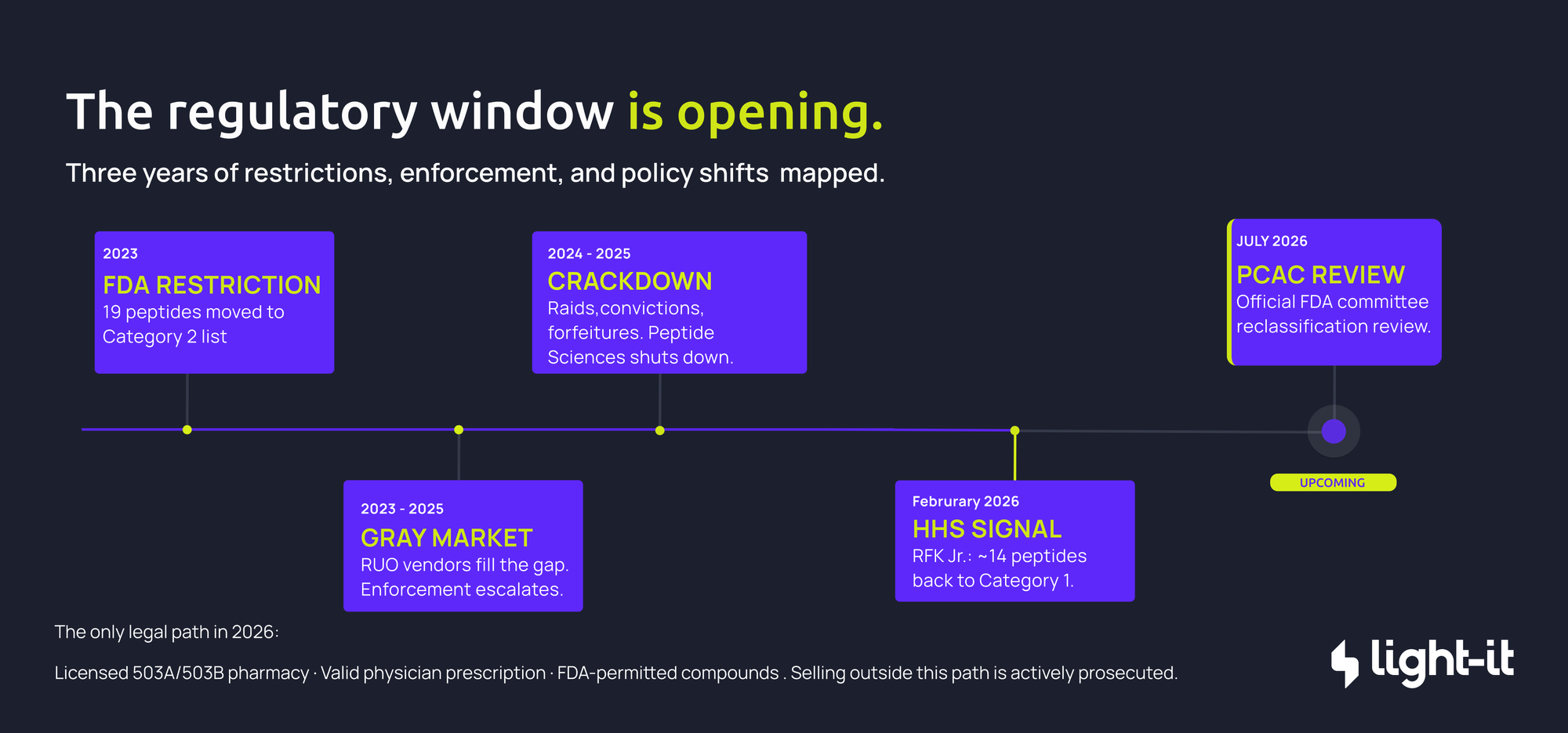

2. The Category 2 Ban and the 2026 Reclassification

In 2023, the FDA pulled 19 of the most popular peptides — BPC-157, TB-500, CJC-1295, among others — off the compounding-permitted list and placed them on the restricted Category 2 list, citing safety concerns, impurity issues, and a lack of clinical data.

Following a February 2026 announcement by HHS Secretary RFK Jr., the FDA removed roughly 14 of those restricted peptides from Category 2 in April 2026. The FDA's Pharmacy Compounding Advisory Committee has meetings scheduled for July 2026 to formally review them for Category 1 placement. Once approved, licensed pharmacies will again be able to prepare and dispense them with a prescription.

3. The hidden economics

When physicians dismiss peptides for lacking human trial data, that absence reflects economics as much as science. FDA approval costs hundreds of millions to over a billion dollars, a bet pharma only makes when there's a patent to protect. Naturally occurring peptides can't be easily patented, so they rarely attract a commercial sponsor. No sponsor, no trials. No trials, no approval. No approval, physicians can't recommend them.

What sits on the other side of that gap is decades of animal studies showing consistent effects across tissue repair, inflammation, neurological function, and metabolic health. Substantial signals, unresolved in humans because the incentive to properly test them never existed.

4. The "Research Use Only" Gray Market: Illegal

When the 2023 restrictions hit, a massive unregulated gray market filled the gap. Online vendors kept selling the same peptides directly to consumers, no prescription needed, by slapping "For Research Use Only" or "Not for human consumption" on the label.

That disclaimer means nothing legally. The FDA classifies products based on intended use, not labeling. If a vendor sells RUO peptides alongside dosage guides and reconstitution instructions, the FDA treats the label as a cover story and the product as an illegally sold, unapproved drug.

5. The Crackdown

The gray market growth triggered an aggressive federal response. Over the last year, enforcement escalated well beyond warning letters: warehouse raids (Amino Asylum), criminal convictions, and multi-million-dollar forfeitures (Paradigm Peptides, Tailor Made Compounding).

The most telling sign of the pressure: Peptide Sciences (widely considered the largest gray-market vendor in the US, pulling an estimated $7.4 million a month) voluntarily shut down in March 2026.

The bottom line: selling peptides as unregulated research chemicals for human use is illegal and being actively prosecuted. People are getting access to these chemicals through Discord and illegal Chinese vendors that ship them. It is important to highlight that the only legal path runs through licensed pharmacies, valid prescriptions, and FDA-permitted compounds.

What does it mean for any digital health company?

What I previously highlighted: technology, regulation, and clinical expertise.

Beyond the hype, the Discord channels and the thousands of influencers, if these compounds have the potential to actually help people, the structure to provide them safely is key for success. Healthcare is about trust and I believe tech can enhance this trust or break it. Players need to treat anything people are injecting on themselves with the seriousness it involves. Clear instructions, good UX, easy but lawful prescription and access are key to become this trend into an actual healthcare solution.

The business models winning in peptide therapy

Peptides is the new word but businesses selling them (GLP-1, NAD+ etc) have been around for a while. A typical flow for a patient entering this market with any digital health company looks something like this:

Considering this, founders or companies that are looking to expand into this sector technically they need the following:

Prescribing & Intake: The most efficient peptide platforms use an asynchronous "store-and-forward" model. The workflow starts with a detailed clinical intake form capturing medical history and contraindications. AI can be incorporated into this step. It can be a simple intake or a more complex one including state laws, specific questions, sync visits or more. For example, an AI-powered triage system can stratify patients into risk tiers: Green for straightforward asynchronous prescribing, Yellow for cases needing lab reviews, and Red to trigger mandatory synchronous video visits. For the prescribing engine, your platform needs to connect to the Surescripts network. Because Surescripts certification requires rigorous testing and DEA audits for controlled substances, never build this from scratch, integrate a pre-certified e-prescribing vendor like DoseSpot, DrFirst, or RXNT.

Compounding Pharmacy Integration: Unlike standard retail pharmacies, many 503A compounding pharmacies still rely on secure fax or direct portal integrations. Your platform must support multi-pharmacy routing logic, since different 503A partners specialize in different compounds or regional shipping. You also need a fulfillment tracking pipeline so patients can follow their order from compounding to quality check to shipment.

An alternative worth evaluating: vendors like Openloop, CareValidate, or Beluga manage pharmacy relationships end-to-end and also provide providers, but typically at a lower margin on medications sold. For platforms serious about unit economics, direct integration with 503A pharmacies (or acquiring a pharmacy license)removes the middleman entirely and can significantly improve per-prescription margins. It requires more operational lift upfront, but at scale it's one of the highest-leverage decisions in the compounding care model.

Billing & Prescription-Gated E-Commerce: Generic e-commerce tools like Shopify create serious compliance risk when paired with a separate EHR: manual checks fail, and patients could end up purchasing compounds they haven't been prescribed. Billing needs to be tied directly to the prescription layer, enforced at the database level so a patient can only see and pay for what a licensed provider has prescribed them, and that access disappears automatically when the prescription expires. For payment infrastructure, Stripe is the most widely used and robust solution for handling this kind of gated commerce.

Monitoring & Labs: Most peptide and longevity protocols rely heavily on biomarkers. Your stack should connect to lab networks like LabCorp, Quest Diagnostics, BioReference, and Getlabs for at-home phlebotomy, so providers can order and track results directly within the clinical record. As the platform scales, monitoring should expand to include remote patient monitoring by integrating wearables like continuous glucose monitors and HRV trackers for continuous data.

All these nuances are key to succeed and ensure a good patient experience. Technical debt is not an option in this business where regulations are constantly changing and updating. Having a partner that can navigate it with you and is up to date.

Final Insights

The market for peptides is real, the clinical interest is real, and the regulatory window opening in 2026 will bring a new wave of founders trying to build in this space. Most of them will underestimate what it actually takes.

The ones who succeed won't be the ones with the most compelling peptide lineup. They'll be the ones who built the right foundation: a compliant prescribing flow, a pharmacy integration that doesn't break when regulations shift, billing tied to the prescription layer, and monitoring that gives providers real data to work with. That's not a nice-to-have stack. In a regulated healthcare environment, it's the only stack that survives.

Technical debt is especially unforgiving here. Regulations around peptides have changed multiple times in the last three years and will keep changing. If your architecture can't adapt quickly, every regulatory update becomes a product crisis.

At Light-it, we've built clinical platforms in exactly these kinds of high-stakes, fast-moving environments. If you're a founder or product leader thinking seriously about the peptide space and want to think through what building this right actually looks like, we'd like to have that conversation.